Sponsored by Battle Quest Comics

By Brian Hibbs

If your memory is good, you may remember the column I wrote almost exactly a year ago titled “We’re one success away from saving comics”. Well, hey, I feel like I got a good part of that right!

The general fortunes of periodical comics has become a rising tide over the last year, between Image/Skybound’s Energon Universe, Marvel’s “Ultimate” and X-Men relaunches, and the end of the year culminating with DC’s “Absolute” line. Very clearly, when you produce the kinds of comics that people want, that brings more of them in to buy those periodicals, and those people get exposed to the entire panoply of material being produced. We still have no sales charts to be able to actually demonstrate the actual specifics of the trends of comic book sales 2024, but I can certainly look to my own anecdotal results for the year and come up with some statements. Yes, I absolutely know and agree that one should never try to present anecdote as fact, but since DC set us down the dark path of fractured distribution, there is really no choice but do that. I am sorry.

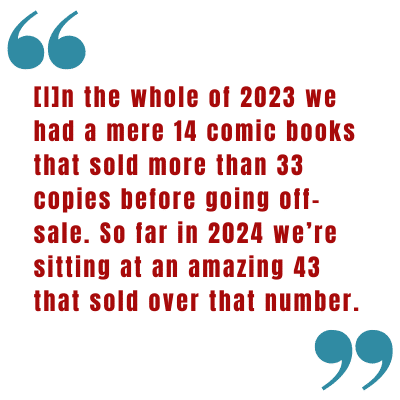

So, anecdote it is: in the whole of 2023 we had a mere fourteen comic book periodicals that sold more than thirty-three copies before going off-sale. And so far in 2024 (with still ten more days as I write this before Christmas), we’re sitting at an amazing forty-three that sold over that number – around a tripling at that benchmark! Sales are up (November was an amazing 24% up, year-over-year), and the busiest days of the season are yet to come. The “best seller” periodical is selling the best it has in years, and that is heartening, because I firmly and fundamentally believe that the pipeline of serialization-to-collection is the best possible path to paying the largest number of creators appropriately for their labor and creations.

So, anecdote it is: in the whole of 2023 we had a mere fourteen comic book periodicals that sold more than thirty-three copies before going off-sale. And so far in 2024 (with still ten more days as I write this before Christmas), we’re sitting at an amazing forty-three that sold over that number – around a tripling at that benchmark! Sales are up (November was an amazing 24% up, year-over-year), and the busiest days of the season are yet to come. The “best seller” periodical is selling the best it has in years, and that is heartening, because I firmly and fundamentally believe that the pipeline of serialization-to-collection is the best possible path to paying the largest number of creators appropriately for their labor and creations.

It’s also probably correct to put a decent chunk of the success of the “Absolute” comics from DC on the net-priced bundles they offered, which really allowed more retailers to go significantly deeper than they otherwise would – again, for anecdote’s sake, this was the key for my store to be able to sell triple digits on a Batman comic for the first time since 2016. The biggest block to maximizing sales in the current market is the trepidation of retailers in taking the Big Swing for inventory (this is also generally true for the publishers, which is why Ultimate Spider-Man #1 went through seven printings, and Transformers #1 is sitting at ten so far), and low-net-priced bundles are a solid tool to frontload stock into stores.

There is still more to do – including open questions about how those publishing initiatives are going to fare in their second years, and if the inevitable line expansions that are going to come from those successes is going to slow demand. And especially in seeing if publishers can find this kind of broad success with something that isn’t just doing a new iteration of already existing IP! At least we’re on a solid base to grow from with comic book sales 2024, which absolutely didn’t feel like the case a year ago. But I feel like the greatest potential problem area now is in the fractioning of, and ultimate viability this then yields for, distribution.

There is still more to do – including open questions about how those publishing initiatives are going to fare in their second years, and if the inevitable line expansions that are going to come from those successes is going to slow demand. And especially in seeing if publishers can find this kind of broad success with something that isn’t just doing a new iteration of already existing IP! At least we’re on a solid base to grow from with comic book sales 2024, which absolutely didn’t feel like the case a year ago. But I feel like the greatest potential problem area now is in the fractioning of, and ultimate viability this then yields for, distribution.

It certainly seems to me that distribution is mostly a numbers game, and that there is actually very little money to be made from distributing the bulk of what is published. Again, we have no more current sales charts, but if we look at the last time we did (March 2020), there weren’t even twenty comics that were selling over 50k then, and by the time you got to the hundredth-best-selling periodical you were on the cusp of dropping under 17k copies sold. Note, too, those reported numbers are including variant covers, but each individual SKU of those variants requires the same amount of labor, data management, tracking, packing, shipping, and so on at the distribution level. If you are splitting those 17k sold across what was 17 different SKUs on item #100, then at least a few of those SKUs are likely to be individual money-losers on the distribution side of the business.

But, as long as distribution was a consolidated business, the largest publications were largely covering the expenses of the misses. This is true in retail as well: my ability to carry onesies and twosies of small press books is absolutely predicated on selling enough top-sellers from the larger publishers. The hits create the ability to stock books that do worse. And this absolutely includes all of the onesies and twosies of the poorest selling comics from Marvel and DC too!

But, as long as distribution was a consolidated business, the largest publications were largely covering the expenses of the misses. This is true in retail as well: my ability to carry onesies and twosies of small press books is absolutely predicated on selling enough top-sellers from the larger publishers. The hits create the ability to stock books that do worse. And this absolutely includes all of the onesies and twosies of the poorest selling comics from Marvel and DC too!

The thing is, for that kind of institutional support to happen, there needs to be a core desire to build your business that way. At Comix Experience we carry a larger amount of well, perhaps we should call it commercially dubious material than maybe is wisest, because we’re dedicated to the medium itself, as a whole – not just to servicing specific IPs. We also know that often something fringe can grow into something mighty when it is given a little love and attention. And as below, so above. I think it is very fair to say that Diamond, as the periodicals distributor with the widest number of publishers and titles, is almost certainly not much above break-even on distribution for a meaningful number of them.

Because I don’t think that the scale of things is really all that understood by many of you, here’s a small breakdown: Penguin Random House (which is the largest distributor of book format material) has effectively a sideline in distributing periodical comics – as of today, they solely distribute Marvel, Dark Horse, IDW, and, coming in July, Boom. That’s just three (and soon to be four) periodical publishers. PRH is not technically exclusive with those publishers: they are allowing Diamond to sub-distribute them (albeit at a worse discount, and charging shipping, while PRH is freight-free)

Because I don’t think that the scale of things is really all that understood by many of you, here’s a small breakdown: Penguin Random House (which is the largest distributor of book format material) has effectively a sideline in distributing periodical comics – as of today, they solely distribute Marvel, Dark Horse, IDW, and, coming in July, Boom. That’s just three (and soon to be four) periodical publishers. PRH is not technically exclusive with those publishers: they are allowing Diamond to sub-distribute them (albeit at a worse discount, and charging shipping, while PRH is freight-free)

Lunar has slightly more: leading with DC and Image, they also stock periodical comics from (and I am using the list for December 2024 data – February 2025 shipping material – for this analysis) eleven other publishers, for a total of thirteen vendors. DC periodicals are totally exclusive (in the US) to Lunar, but Image are also sub-distributed by Diamond – note that this is for periodicals, and initial orders only for graphic novels. Diamond does not wholesale any restock of graphic novels from Image.

Diamond, on the other hand, is the sole source for periodicals from 63 different publishers. They have “exclusive” deals with a handful of those (it’s under a dozen, I think, though there’s not a quick way to look that up that I can spot), but they’re otherwise effectively the exclusive distributor for all of those 63. They also sub-distribute initial orders of all of the PRH material, and, as noted, Image from Lunar.

So, while there are sixteen (soon to be seventeen, come July when Boom! moves to PRH) publishers whose periodical comics can be bought somewhere else than Diamond (and only one – DC – that can not), there are nearly four times as many publisher’s releases that cannot be bought from any distributor other than Diamond, in the US. Again: this is using DEC24 data for this calc, and February is usually the slowest shipping month of the year, so that number of publishers is possibly actually 20%+ higher.

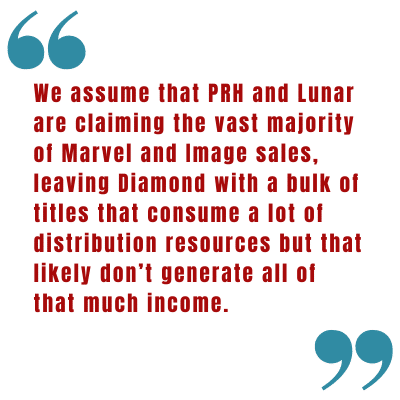

Here’s the thing, though: Marvel, DC and Image are, combined, roughly 80%+ of all of the volume of periodical comics sold, and we assume that PRH and Lunar are claiming the vast majority of Marvel and Image sales, leaving Diamond with a bulk of titles that consume a lot of distribution resources but that likely don’t generate all of that much income.

Now, I’m fairly certain some of you will say, “Well, those other 63 publishers will just sign deals with PRH or Lunar, obviously!”, but I’m equally certain that this is not even remotely correct. My understanding from publishers that I have spoken to is that on the PRH side they are not taking any additional clients (at least not with some pretty major concessions), and on the Lunar side, they simply don’t appear to have the bandwidth or resources to take on more vendors, at least to handle them correctly. Many of the not-DC and -Image publishers have shared stories with me of Lunar’s operation that don’t sound very good, though it’s not my place to tell these tales out of school. Even with Image, I can see from my side of the counter that they’re, even after six months of being Image’s primary distributor, having significant problems with inventory control and accurate data.

Even putting aside something as basic as access-to-the-market, Diamond also does a lot of things that no one else does nearly as well, including physical catalogs, data services and maintenance of entirely key operations like the assignment of “series codes” (the thing that lets your local comic book store pull and maintain your comics subscriptions), operating and marketing Free Comic Book Day, not to mention having a “one stop shop” for not only comics, but all of the toys and trading cards and etc that Diamond stocks that neither PRH or Lunar are anywhere near being in the business of distributing. I’d say that there’s far more that Diamond does to maintain the entire eco-system of the comic book industry than they even slightly get credit for. They’ve also spent four decades being the “bank” for comics retailers in a way we already know for a fact that PRH will not be willing to do, and that Lunar doesn’t appear to have any of the resources to accomplish.

I certainly don’t want to pretend than Diamond is a flawless distributor (cuz, wow that would sure not be a true statement!), but given the scale and scope of their operation and all of the myriad of ways they give access to so many vendors, it would be a horrifying nightmare for the vast majority of publishers, and for the entire state of periodical comics, and all of the efficiencies that distribution brings, if Diamond went under. Mark my words, it will not be viable for the overwhelming majority of small press publishers and independent comic book stores to not have a centralized distribution system. Many many things will collapse if Diamond fails, and the options for creators for viable access to the market will shrink radically.

I certainly don’t want to pretend than Diamond is a flawless distributor (cuz, wow that would sure not be a true statement!), but given the scale and scope of their operation and all of the myriad of ways they give access to so many vendors, it would be a horrifying nightmare for the vast majority of publishers, and for the entire state of periodical comics, and all of the efficiencies that distribution brings, if Diamond went under. Mark my words, it will not be viable for the overwhelming majority of small press publishers and independent comic book stores to not have a centralized distribution system. Many many things will collapse if Diamond fails, and the options for creators for viable access to the market will shrink radically.

And this is the thing that terrifies me the most: Diamond has shown a lot of bad signs over the last few months that leave me with serious questions for their ongoing viability.

The first thing that scared me is that sometime in July or so Diamond appeared to be cut off from Hachette (one of the “Big Five” of book distribution) – which includes their owned imprints of Yen Press, Little Brown, etc, in addition to publishers they “just” distribute like Chronicle and Abrams. For months, zero new product was flowing into Diamond from Hachette, all with literally no communication whatsoever from Diamond about the circumstances. This appears to have been settled now, after approximately four months of product stopping, but what I was hearing from back channels was that there were payment issues at the core. Historically, Diamond has been flawless about paying, as far as I know, so seeing a major vendor cut them off entirely was… well, concerning, to say the least.

The second major issue this quarter is that Diamond suddenly closed one of their two warehouses, which they are communicating was a result of their landlord changing plans at the last minute, but it has caused truly dire problems with getting material shipped – we’re now on the fourth week running that new products from Diamond, nationally, are not arriving into stores until after the start of business on Wednesday new comics day. This is a major issue, costing many retailers a lot of time and energy at the time of the year that product really really should be flowing smoothly, and costing publishers sales days and their best windows of operations. In addition, many retailers are complaining about how invoicing is working from Diamond right now, with many saying they are getting multiple, contradictory, invoices each week. There’s not even product tracking information coming from Diamond. It’s infuriating.

These are not good things, and while they may be unrelated, it is causing a whole lot of retailers to be talking about moving as much business from Diamond as they can – especially folks who have been holding on to Diamond for centralized Marvel, Image, IDW and Dark Horse periodicals. At a certain point, the math will change out that Diamond will be in genuine trouble from these kinds of problems.

The state of the (periodical) market is in flux right now – much is going right, but the viability for anything but the biggest players seems more in question than ever before. What a way to go into 2025!

Hey, next column will be the 2024 BookScan review, and, wow, column #300! See you in a few months!

Brian Hibbs has owned and operated Comix Experience in San Francisco since 1989, was a founding member of the Board of Directors of ComicsPRO, has sat on the Board of the Comic Book Legal Defense Fund, and has been an Eisner Award judge. Feel free to e-mail him with any comments. You can purchase a collection of the first Tilting at Windmills (originally serialized in Comics Retailer magazine) published by IDW Publishing, as well as find an archive of pre-CBR installments right here.

Sponsored by Battle Quest Comics

{kind=link}

Two days after Brian posted this, and still not a single reaction? I guess retailers must be busy. Or maybe they are afraid to admit that Brian might be right, and Diamond’s days are numbered. I for one sincerely hope this is NOT the case, as Brian very clearly demonstrates that the effect to the Industry of losing Diamond would be just as horrible as losing Capital Distributions was in the mid nineties.

I do find the Hachette debacle, and the complete lack of communication by Diamond in this matter, very disturbing. The fact that this has been going on since mid-Summer makes it clear that the Warehouse Closure operation wasn’t just streamlining, but a move that was absolutely necesarry for Diamond to (hopefully) be able to survive the near future. Now the operation has blown up in their face, they need to ship books as fast as possible, cause if they don’t ship, they don’t get to bill their customers. They risk losing whatever they’d hoped to save on the Warehouse costs to additional labour costs, delayed payments because of delayed shipments, and damage replacements for books damaged during relocation.

I also do not understand why Diamond isn’t able to prosper more from the manga boom. But this seems to be never in the discussion when Diamond is considered. Of all the companies you don’t pay, you don’t pay the one providing you with The Guy She Was Interested In Wasn’t a Guy At All, Bungo Stray Dogs, Delicious in Dungeon and Solo Leveling? Is the amount of Diamond’s accounts total ordering of manga so low, that it’s more worthwhile to keep on paying Dynamite for variant covers A through Z and beyond, but you leave Solo Leveling GN Vol 10, or The Guy She Was Interested In Wasn’t a Guy At All GN Vol 01, or the Delicious in Dungeon Box Set to the competition?

I did not have a chance to read this til now. I am on vacation in Cancun. I buy everything through Diamond, except Dcs. If Diamond dies, I will switch to other distributors or just start selling the 250,000 books I have in storage on my now 8 year old Facebook Live page, facebook.com/groups/livecomicsale. I am more worried about tthe future of the USA, then the comic book industry.

Yes I do suspect Diamond’s days are numbered, but that is unfortunately no fault of anybody but Diamond. There is a whole lot they just refused to do over the last 25 years that many people told them they should be doing – for their own benefit. Brian knows this better than anybody. Like straws on a camels back it eventually broke them, at least for comics.

Comments are closed.